4 ways to pay off your mortgage faster

December 2, 2025

If you’re a homeowner with a mortgage, it’s very likely that you’ve Googled ‘how to pay off my mortgage ASAP’ at some point. We get it. Owning a home: goals. Paying off a mortgage: Not as exciting. That’s why we’re giving you 4 ways to pay off your mortgage faster and achieve your mortgage-free goals even sooner.

Accelerated payments vs. regular payments

The simplest way to chip away at your mortgage faster is by changing how often you make payments. The more frequent your payments, the less interest you’ll end up paying and the faster your mortgage will be paid off. If you’re really looking to fast-track your mortgage payments, most lenders offer an accelerated payment option, such as accelerated bi-weekly or accelerated weekly payments.

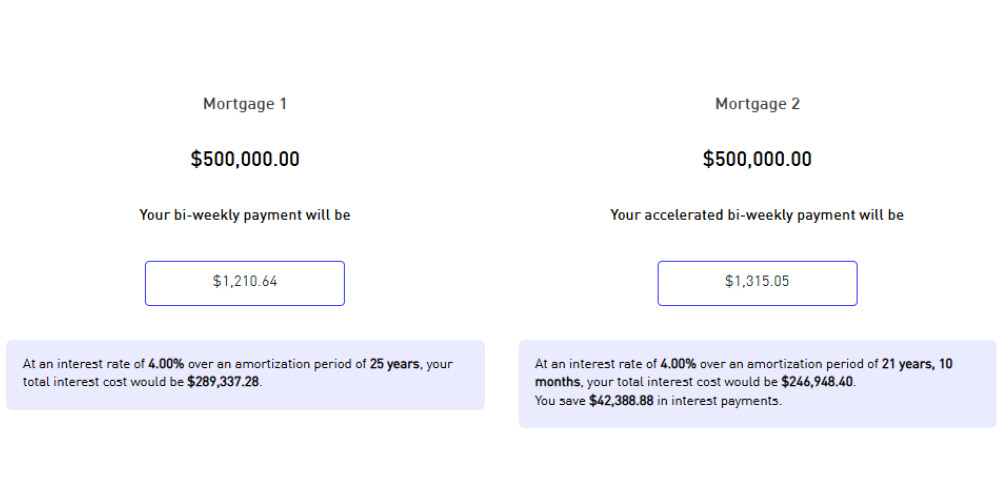

Bi-weekly payments and accelerated bi-weekly payments are calculated differently. Here’s a quick breakdown:

Regular bi-weekly Multiply your regular monthly payment by 12, then divide by 26 |

Accelerated bi-weekly Divide your regular monthly payment by 2, and then multiply it by 26. |

Because of this difference in how the payments are calculated, with the accelerated option, you end up making the equivalent of one additional monthly payment in a year. That really adds up over time! That single extra payment can shave years off your mortgage and save thousands in interest.

Let’s compare payments

Try out our mortgage calculator and see how accelerating your mortgage payments could make a difference!

Make lump-sum payments when you can

Got a bonus, tax refund, or some extra savings? You can put that money to work by making a lump-sum payment directly toward your principal. Most lenders allow you to make lump-sum payments, often up to 10–20% of your original mortgage amount per year, without penalty. Even small lump sums can make a big difference over time by reducing the balance that your interest is calculated on.

Let’s say you had a mortgage balance of $500,000 at a rate of 5.00% with a 25-year amortization, and you were to make an annual lump sum of $2,000 on top of your regular monthly mortgage payments. By the end of the amortization period, you’d save $44,617.78 in interest and pay off your mortgage 31 months sooner!

This Mortgage Calculator from the Government of Canada is super helpful in breaking down how different lump sum scenarios can help you reach your mortgage payment goals.

Pro tip: Schedule lump-sum payments annually around bonus time or tax season — it’s an easy habit to build.

Round up your payments

Rounding up your payment may not sound like much, but it’s a low-effort, high-impact strategy.

For example, if your mortgage payment is $1,263/month, round it up to $1,300 or even $1,350. The extra $37 – $87 goes straight toward your principal each month, helping you reduce your balance faster without a major change to your budget.

Over time, those small top-ups can cut months or even years off your amortization.

Lump sum payments vs. Increasing your paymentsLump sum payments are a great option because they’re flexible! But it’s important to remember that if you choose to increase your regular mortgage payments, you can’t switch back to the original amount. Be sure to double check your budget and make sure the increased amount will work for you. If you’re not sure if a consistently higher payment is the right route for you, side aside the additional amount in a savings account for a couple months or a year and see how it feels. You can still use that money to make a lump sum payment later on without the full-on commitment.

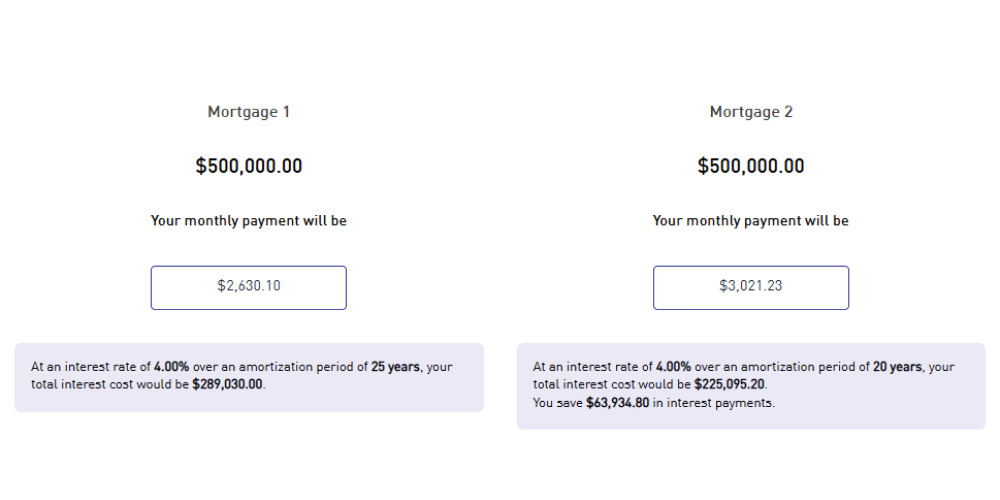

Renew strategically: Avoid extending your amortization

When it’s time to renew your mortgage, it can be tempting to reset your amortization period to 25 years again. But that’s almost like taking a step backward when you’re trying to reach that mortgage-free finish line.

Instead, if you’ve already paid down a few years on your mortgage, consider shortening your amortization — say, from 25 years to 20 years. Your payments might increase slightly, but you’ll pay off your mortgage faster and save significantly on interest in the long run. Think of it as a financial “reset” that keeps your goals in focus.

Lengthen Amortization

|

Shorten Amortization

|

Finding a mortgage payoff method that works for you

Now that you’ve got some info on different ways to reach your mortgage-free goals even faster, you might be wondering, ‘Which one is right for me?’ Almost all of the options we’ve gone over could work for any homeowner, but it really comes down to your lifestyle, preferences, and overall goals.

For someone who wants to pay down their mortgage yesterday or as soon as possible, they may be willing to make some drastic lifestyle changes to devote funds towards lump sum payments throughout the year. Whereas someone who is working with a more limited budget may prefer adding an extra $25 to each mortgage payment for a slow and steady climb to reach their goals. Whatever you choose, make sure it not only helps you reach your goals but helps you live the life you want to live!

If you’re not sure which strategies make the most sense for your situation, a mortgage professional can help you find the right balance between saving interest and keeping your payments manageable. If you’re an existing MERIX homeowner, contact us and we’d be happy to help.

Your mortgage-free future could be closer than you think!